- About Us

- Our Products

- Resources

Tue • Aug 11, 2026, 13:18:24 GMT+1

REGULATIONS SHAPING DIGITAL CONSUMER LENDING IN NIGERIA IN 2026

Nigeria's 2026 digital lending is shaped by Open Banking, FCCPC DEON & NDPA GAID. Get the full breakdown, timelines, and what they mean for lenders

Business, Strategy & Transformation Office

May 01, 2026. 3 mins read

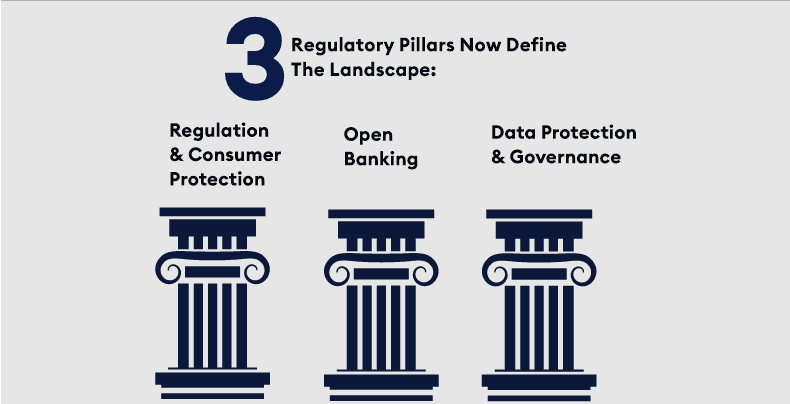

Nigeria's digital lending space is now governed by a comprehensive, structured regulatory framework. Three interlocking pillars — Open Banking, Consumer Protection (DEON), and Data Governance (NDPA/GAID) — define the operating standards for 2026, creating clearer rules for lenders and stronger protections for consumers.

Whether you're a fintech startup, a microfinance bank, or an established digital lender, understanding and aligning with these frameworks is essential this year.

Three Regulatory Pillars Reshaping the Market

1. Open Banking

Structured Approach to Data Sharing:

The CBN's Open Banking Framework, now rolling out in phases, establishes standards for how lenders share and access customer data through APIs. Access is governed by a Risk-Based Tiering Model, meaning the level of data a lender can access is tied to their regulatory standing and risk management maturity. Lenders registered on the CBN Open Banking Registry and equipped with compliant API infrastructure are positioned to benefit from richer data access and improved credit decision-making.

2. FCCPC DEON Regulations

Broadened Oversight for Digital Credit:

The Federal Competition and Consumer Protection Commission (FCCPC) has extended its regulatory scope to cover every entity offering unsecured digital credit, beyond just mobile apps. As of February 2026, over 400 digital lending companies fall under its jurisdiction. The final regularization deadline was April 30, 2026, with penalties of up to ₦100 million or 1% of annual turnover applicable to non-compliant operators. The framework also introduces clear standards around pricing transparency, ethical debt recovery, and complaint handling, raising the bar for consumer experience across the sector.

3. NDPA & GAID

Data Governance Gets More Operational:

The Nigeria Data Protection Act (NDPA), now operationalized through the 2025 General Application and Implementation Directive (GAID), establishes a clear and practical framework for how lenders must handle customer data. Lenders are required to collect only necessary data, establish a lawful basis for processing, appoint certified Data Protection Officers, and report breaches within the stipulated time.

Why This Matters Beyond Compliance

These regulations present real opportunities for lenders who engage with them seriously. Open Banking enables better credit scoring through consented, real-time data access. The DEON framework creates a more level playing field that rewards transparent, ethical operators. And strong data governance builds the kind of consumer trust that supports long-term growth.

Lenders who align their infrastructure and practices with these frameworks are better positioned to compete, innovate, and serve customers well.

The Bottom Line

Nigeria's regulatory environment is becoming more defined, and that clarity benefits the entire ecosystem — regulators, lenders, and consumers alike. The convergence of Open Banking, consumer protection standards, and data governance reflects a deliberate effort to build a more transparent, inclusive, and well-governed digital lending market.

The full report from Princeps Credit Systems Limited breaks down each regulatory pillar in detail, including compliance timelines, tiering models, framework comparisons, and a practical action checklist for lenders.

Get all these directly to your inbox.

Leave a comment

ongoing conversations

No comments yet

Be the first to share your thoughts on this article.

Let's chat; Kindly fill out this form and we will respond in less than 24 hours.

Our core values as a company reflects beyond just us doing business; Excellence, integrity, humility, professionalism, trust and empathy is in the gene of every Princeps Star!